The Labour Party wins UK general election, securing a landslide majority. Analysts see positive implications for UK assets and economy.

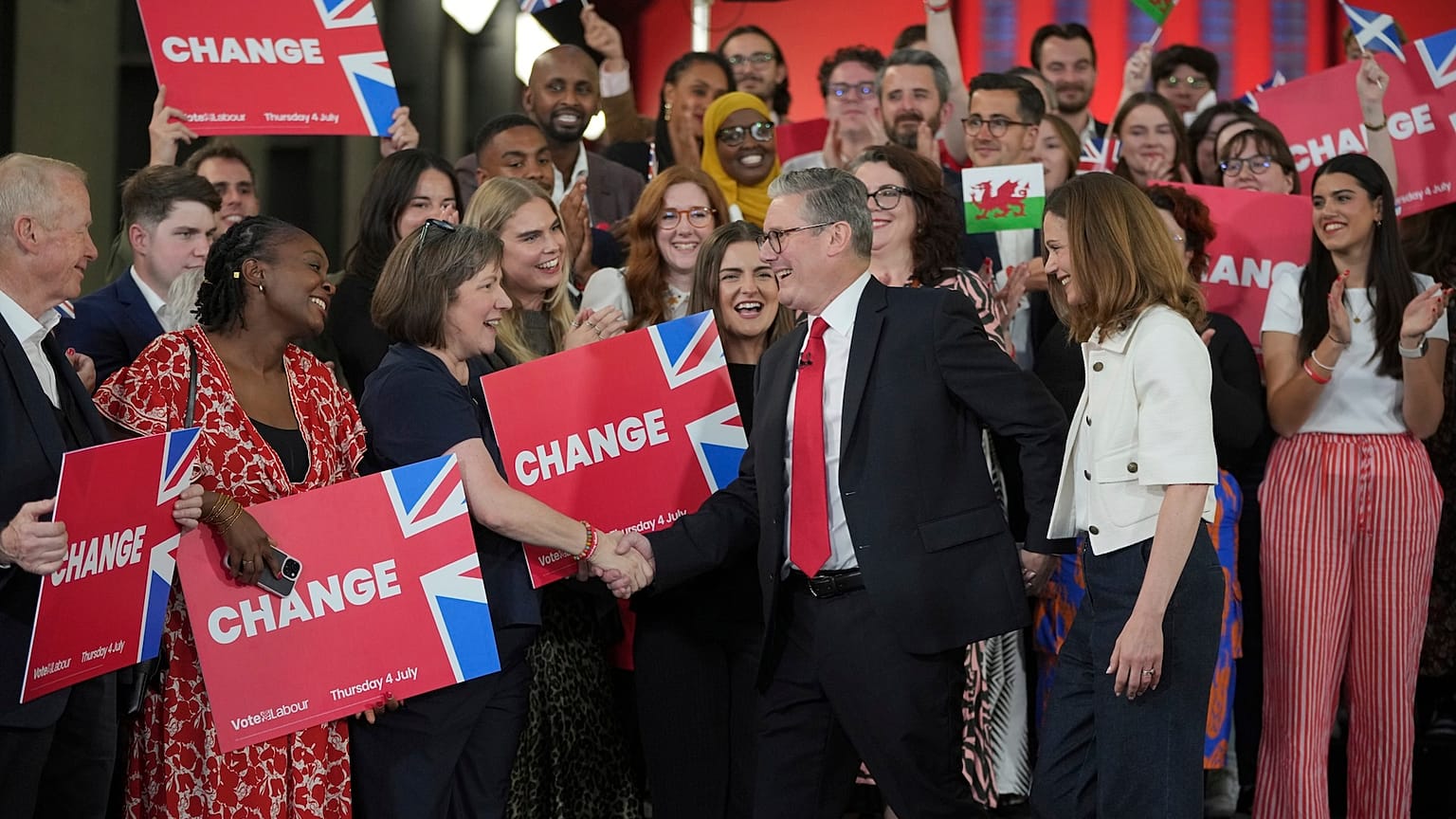

In a seismic shift for the UK's political landscape, the Labour Party has secured a landslide victory in the 2024 general election, winning 410 seats and marking a significant increase of 212 seats from the 2019 elections.

After being invited to form a government by the UK's Head of State, King Charles, Labour Party leader Keir Starmer will head to 10 Downing Street, ending the Conservatives' 14-year tenure.

The Conservative Party has experienced a dramatic loss, reducing their representation to just 119 seats, a decrease of 249 seats. The Liberal Democrats have made notable gains, securing 71 seats, an increase of 63 from the previous election.

This result gives Labour a comfortable margin above the 326-seat majority threshold, enabling them to pass legislation needed to implement their political manifesto.

Market reactions

Financial markets had largely anticipated Labour's decisive victory, and initial reactions were relatively subdued.

The British pound rose only by 0.1% to 1.2770 against the dollar at 09:30 CET on Friday, but still continuing its six-day upward trend. The euro remained nearly unchanged against the pound at 0.8472.

Gilt yields saw a slight decline, with the two-year yield at 4.15%, marking its sixth day of easing in the last seven sessions. Long-dated 10-year gilt yields also fell by two basis points to 4.18%, although they have risen from their June low of 4%.

The FTSE 100 index opened 0.4% higher, with small caps leading gains. Persimmon, Barratt Developments, and Taylor Wimpey rose 3.1%, 2.4% and 2.3%, respectively.

The positive sentiment in the UK equity market extended to broader European markets.

The Euro STOXX 50 index rose by 0.5%. In France, stocks were 0.4% higher ahead of Sunday's second-round legislative election. In Germany, the DAX index was 0.6% higher. Tyre producer Continental surged by more than 2% following a recommendation upgrade from JPMorgan.

Analyst perspectives on UK elections

James Smith, UK economist, ING Group:

"The new government faces enormous financial and fiscal challenges. Elevated gilt yields reflect the fact that public debt is within spitting distance of 100%, and the deficit is at 4.4%."

Smith added that the Labour Party "will inevitably need to go beyond what it promised during the campaign" and has made clear its intent to avoid further austerity.

Smith suggested that the new government might find it easier to secure extra cash in its first budget than many expect. "Small edits to the fiscal rules and several tweaks to minor taxes and associated reliefs could deliver the money needed to end planned cuts to spending."

Britain's first-ever female Chancellor of the Exchequer (chief finance minister), Rachel Reeves, is expected to take office. The lack of drastic changes to public finances means the Bank of England can proceed with cutting interest rates. "Markets are pricing a 60% chance of an August rate cut, but we think that's too low. Our call for an August cut is the main reason for expecting a weakening in sterling."

James Moberly and Sven Jari Stehn, economists, Goldman Sachs:

"Labour would likely have to increase spending by £14bn a year more than assumed by the end of the Parliament to prevent departments' spending from falling in real, per capita terms."

Labour has pledged closer UK trade and security ties with the EU to mitigate some of the economic costs of Brexit. Moberly and Stehn expect "slightly stronger near-term growth and slightly higher inflation under a Labour majority."

They believe the implications for the BoE would be limited, but there are "risks of slower rate cuts if Labour delivers a sizeable increase in the Living Wage."

Ipek Ozkardeskaya, analyst, Swissquote:

Ozkardeskaya emphasised that, with Labour's substantial majority, small and medium-sized British stocks are likely to benefit more than the larger FTSE 100 Index, which is significantly influenced by global market dynamics and has a heavy weighting in energy and mining sectors.

Luca Cigognini, market strategist, Intesa Sanpaolo:

"The Cable (GBP/USD) has maintained a bullish tone and continues to hover near the resistance level of 1.2780. A break above this level could see it return above 1.2800 and revive sterling's ambitions towards 1.2860, the high from 12 June."

Roberto Cobo, BBVA strategist:

"Starmer is widely seen as market-friendly and orthodox in terms of fiscal policy. Moreover, the markets –and we –are confident that the new government will be vigilant to avoid the kind of chaos that occurred two years ago, when the mini-budget crisis caused UK gilts to skyrocket."

Going forward, BBVA believes that macroeconomic data and the Bank of England's monetary policy will be the primary domestic factors influencing the pound. For the summer and the rest of the year, they are bearish on the pound, anticipating a 25bp rate cut by the BoE in August, which is not yet fully priced in. "We see EURGBP rising to levels of 0.86-0-87 in the coming months," Cobo wrote.