This week, investors will closely monitor the market reactions to the French election in Europe. Additionally, both China and the US are set to release their Consumer Price Index (CPI) data, providing insights into the inflation trajectory of the world's two largest economies.

Apart from a slew of important economic data set to be released by major European countries, market reactions to the French election will be particularly scrutinised this week. Additionally, both the US and China are poised to release their inflation data for June, offering clues for the respective central banks' policy outlooks.

Europe

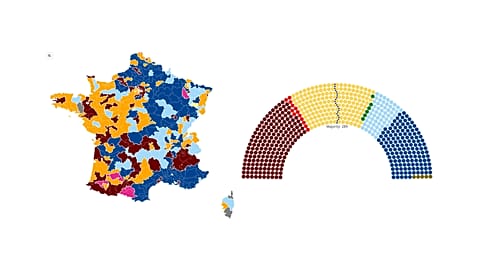

The outcome of the French election may significantly impact both the stock markets and the euro in the region. Equities and the single currency could see further rebound if the far-right National Rally party does not gain enough votes to form a government. However, history shows that elections may only temporarily influence financial markets. Post-election policies and economic development tend to shape the market's long-term trends.

On the economic front, Germany will release its trade balance for May and the Wholesale Price Index (WPI) for June. The German trade surplus decreased slightly to $22.1 billion (€20.36 billion) in April from $22.2 billion (€20.45 billion) in the previous month due to a smaller increase in exports compared to imports. Notably, exports to the UK and Russia surged, while sales to the US fell. The trade surplus is expected to further drop to $19.9 billion 218.33 billion) in May, according to consensus.

Germany's WPI is a key indicator for inflation, as wholesale prices are usually passed on to consumers. The index decelerated in May, increasing only by 0.1% month-on-month, suggesting the country's inflation was on a downward trend. Last week, the prelim CPI showed that German inflation cooled to 2.2% in June after rising for the previous two months. Consensus suggests that wholesale prices may climb by 0.2% in June from the previous month.

Accompanied by similar economic trajectories in the other European economies, these data offer encouraging signs for the ECB to continue its rate-cutting cycle, thereby providing bullish factors to the stock markets.

In the UK, the monthly gross domestic production (GDP) for May is due for release on Thursday. The economy resumed growth in the first quarter from a technical recession in the second half of 2023. According to Forex Factory's survey, the country's GDP may grow 0.2% month on month in May, recovering from a flat growth in the previous month.

The US

Two economic events and data will be in the spotlight for global markets this week – Chairman of the Federal Reserve (Fed), Jerome Powell's testimony, and the US CPI for June. Chair Powell's testimony before the Senate Banking Committee is a critical event for Wall Street and global markets. In this session, Powell will answer the Committee's questions about US economic conditions and the according Fed's monetary policy. Unexpected questions or answers could lead to market volatility.

The US CPI data will be particularly focused, providing clues of the country's inflation trajectory. The consumer price rose 3.3% year on year in May, cooling for 3.4% in the previous month, and 3.5% in March. The retreating trend is promising for the Fed to start cutting the interest rate in September, which would be the first time since March 2020, when the pandemic happened. Further easing price pressure will likely drive Wall Street higher. Consensus calls for a 3.1% year-on-year price increase in June, suggesting that inflation cools in a sharper pace.

Additionally, the Producer Price Index (PPI) is also an important indicator of inflation, representing the factory gate price movement.

The US will kick off earnings season with big banks, including Citigroup, JPMorgan Chase, and Wells Fargo. The financial sector is a bellwether for global economic health due to close connections between these big lenders.

Asia Pacific

China's CPI data for June posts significant importance for consumer demand as the country faced economic challenges due to its property crisis and post-pandemic recovery. On a positive note, China's inflation rose for the third straight month in May, suggesting Beijing's efforts to shore up its economic growth have taken effect. In June, economists expect that China's consumer price will increase by 0.4% annually. The data may further boost commodity prices, indicating positive economic activities in the world's second-largest economy.

Elsewhere, the Reserve Bank of New Zealand (RBNZ) is set to decide on its Official Cash Rate (OCR), with expectations that the bank will keep the rate on hold at 5.5% for the eighth straight time. The bank remained hawkish in its last meeting in May, signalling that interest rates may be at a restrictive level for longer than anticipated. New Zealand only reports quarterly CPI, which was 4% year on year in the first quarter, remaining well above the RBNZ's targeted level of 1-3%.