European stock markets recoup most of their losses from earlier in the week following the release of US CPI data. Regional markets opened lower despite the Fed’s rate decision propelling Wall Street to all-time highs overnight.

European stock markets started the trading session lower on Thursday morning with France's CAC 40, Germany's DAX and the FTSE 100 in London all opening in the red despite resuming their rally on Wednesday.

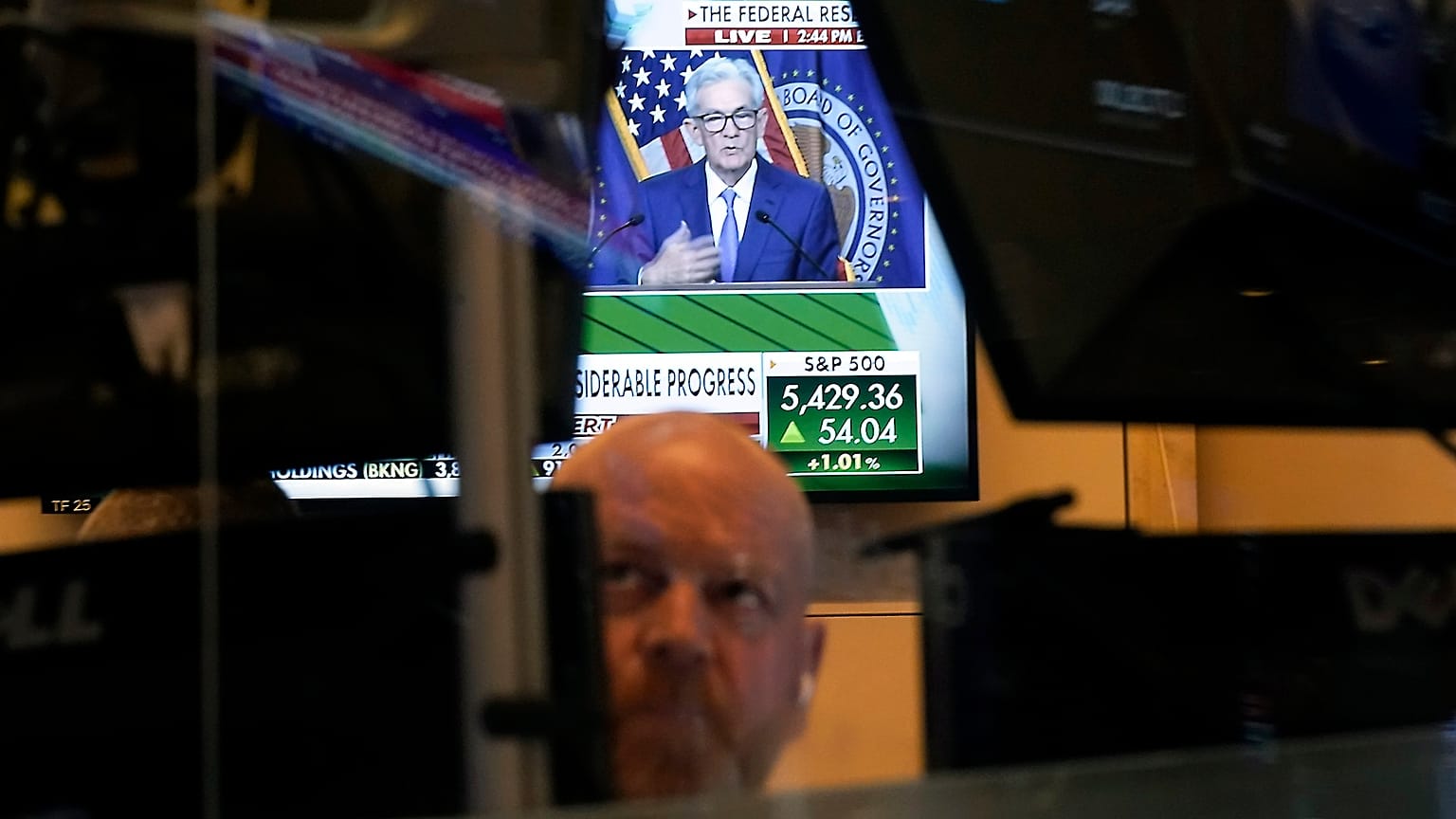

Tech stocks took the lead following cooler-than-expected inflation data from the United States while major benchmark indices reversed losses caused by election jitters earlier in the week, with the Euro Stoxx 600 up by 1.01%, the DAX rising by 1.49%, and the CAC 40 climbing by 0.97% on Wednesday. The rebound suggested that the decline in the European markets provided an opportunity for dip-buyers amidst central banks' rate-cut trajectories.

Central banks on rate cut trajectories

The Fed kept its benchmark rate unchanged at between 5.25% and 5.5% following cooler-than-expected US inflation data on Wednesday. The dot plot, a visual representation used by the Federal Open Market Committee (FOMC) to convey its members' projections for future interest rates, indicated that there would be one rate cut this year and four in 2025. Despite the slower-than-expected rate cut path indicated by the Fed, the central bank confirmed that it was on a rate cut trajectory. Chair Jerome Powell said: "There are fewer rate cuts in the median this year, but there's one more next year".

Last week, the European Central Bank (ECB) delivered the first interest rate reduction since 2019. Despite maintaining a hawkish stance, this move may signify the end of the current rate hike cycle by the ECB. In the same week, the Bank of Canada (BOC) also lowered its policy rate amid cooling inflation and concerns about an economic slowdown. In March, the Swiss National Bank (SNB) was the first central bank to cut its interest rate.

The Bank of England (BOE) is poised to decide on the interest rate next week, with expectations that it will follow the ECB in reducing its policy rate from 5.25% to 5%. Governor Andrew Bailey indicated that a rate cut before the general election could be assured in May. However, the snap election on 4 July called by Prime Minister Rishi Sunak could bring about the first cut as early as next week.

Bond traders project more cuts this year

The Fed's policy meeting triggered a sharp decline in global bond yields due to expectations for central banks to be on track with a rate cut trajectory in the second half of this year, given a positive correlation between interest rates and bond yields. According to the CME Fed Watch Tool, probabilities for a rate cut in September and December are 56% and 42% respectively, suggesting bond traders believe there might be more than one cut this year.

The US 10-year government bond yield dropped by 10 basis points, or 0.1%, to 4.31%, leading to a similar movement in the European markets, particularly in the UK. The British 10-year gilt fell by 14 basis points to 4.13%, the lowest in nearly a month. The country reported flat GDP growth in April, which reinforced expectations that the BOE will commence a rate cut next week. Major government bond yields in the Eurozone also followed the global trend, with the 10-year German bund yield dropping by 9 basis points, and yields on its French and Italian counterparts falling by 9 and 15 basis points respectively.

As bond yields move inversely with bond prices, the rally in bond markets indicates central banks are easing liquidity, which could continue to buoy risk assets, particularly equity markets.

Technology stocks lead markets to gain

A notable trend is that technology stocks led to broad stock market gains on both sides of the Atlantic on Wednesday. Technology stocks are considered growth stocks, with the sector usually benefiting from lower interest rates due to its sensitivity to corporate debt levels.

In the Euro Stoxx 600, major tech companies outperformed the benchmark, with ASML up 2.75%, SAP SE jumping 3.42%, and Siemens AG rising 3.27%. European stock exchanges closed before Wall Street, so the regional markets preemptively reacted to optimism regarding expectations of a rate cut by the Fed.

On Wall Street, Apple surged for the second consecutive trading day after the tech giant announced its long-awaited adoption of artificial intelligence at WWDC4 on Monday. This tech rally propelled both the S&P 500 and the Nasdaq to new highs.

With more central banks potentially commencing their rate-cut cycles in the rest of the year, global stock markets, including those in Europe, are expected to sustain their upward trends. However, this expectation hinges on the absence of an economic recession in the near future. It's worth noting that European markets may not exhibit as robust a performance as their US counterparts due to their lower weighting of technology companies and prevailing political uncertainties.